Small businesses are both the backbone of the U.S. economy and one of its greatest insurance challenges. Recent studies show that the majority of small businesses are underinsured, with many owners unaware of critical coverage gaps.

The Economic Paradox of Small Commercial Underwriting

This issue is compounded by the economic paradox of small commercial underwriting: the processes required to quote, bind, and service policies are nearly identical to those in larger middle-market accounts, yet premiums are far lower. Also, small business accounts generate a similar volume of endorsements and policy changes. These and other elements combine to hinder commercial insurance profitability.

Artificial intelligence creates a path forward by reducing acquisition costs, tailoring products, expanding market access, and enabling insurers to serve small commercial clients profitably while improving coverage adequacy – more quickly without the heavy administrative burden traditionally placed on underwriting and processing teams.

Why Now: A Market at an Inflection Point

The small business market is enormous. According to the U.S. Small Business Administration, there are over 36 million small businesses employing nearly 46% of the private workforce. In insurance, “small commercial” is generally defined as businesses with less than $25 million in annual revenue, under 50 employees, and policy premiums that typically fall below $100,000. This segment is not only the lifeblood of local economies but also represents one of the largest growth opportunities for insurers.

At the same time, the risks facing small businesses are intensifying. Inflation has driven up replacement costs for property. Rising litigation expenses have made liability claims more costly. Supply chain disruptions continue to create ripple effects, leaving many firms vulnerable to business interruption exposures they have never encountered before. In this environment, being underinsured is more dangerous than ever.

State regulators and industry trade groups are also beginning to sound the alarm. Many have highlighted the financial fragility of small firms lacking adequate protection, particularly after natural catastrophes, cyber incidents, or prolonged economic downturns. For insurers, adopting AI not only reinforces our commitment to protecting customers’ wellbeing, but also opens a strategic opportunity to innovate small business insurance solutions – driving profitability while better serving an underserved market.

The Scale of Challenges Facing Small Business Insurance

A business insurance report revealed that 92% of small businesses have business insurance but only 13% of them feel prepared for risk. Even more troubling, other surveys suggest that up to 90% of small business owners lack confidence in the adequacy of their insurance coverage.

The implications of this are twofold. First, small businesses, many of which operate on thin margins, face heightened vulnerability in the event of a loss. Second, insurers risk reputational damage and increased claims severity if coverage gaps remain unaddressed.

The coverage picture is fragmented: only 65% of small firms hold general liability coverage, fewer than half carry property insurance, and only one-third maintain professional liability protection. Too often, owners purchase insurance at launch but fail to update limits and coverages as operations expand. This creates persistent mismatches between exposures and policies.

From an insurer’s perspective, the small commercial insurance business paradox of more overhead with less revenue often discourages carriers from devoting substantial underwriting resources to smaller risks, even as these accounts represent a critical growth segment. Addressing this profitability imbalance between small and middle-market accounts requires operational innovation – and increasingly, that innovation is driven by artificial intelligence.

AI as an Efficiency and Growth Lever for Small Business Insurance Operations

AI gives insurers the tools to reduce costs, improve underwriting precision, and expand access to underserved markets. Areas where insurers are successfully improving the efficiency of their small-business insurance operations include:

- Lower acquisition and distribution costs: AI analyzes business profiles and market data to more effectively identify and target underinsured companies, allowing insurers to reach the right prospects at scale while keeping marketing and distribution costs in check. Automated outreach and tailored campaigns help make small commercial accounts profitable, even with modest premium revenue.

- Personalized products and dynamic pricing: AI rapidly evaluates companies' operations, size, and risk profile to recommend the right mix of coverages and appropriate limits. It can also adjust pricing to reflect business changes, such as growth in revenue or staff. In real time. This creates more responsive protection for policyholders and more accurate pricing for insurers.

- Expanded market access and education: AI can help customers feel more at ease and more informed. Virtual assistants and chatbots already outperform human customer service agents, answering policy questions in plain language, guiding business owners through coverage options, and prompt them to update protection as their operations grow. This improves customer confidence while allowing agents and brokers to focus on higher-value advisory work.

Aligning With Underwriting Mandates

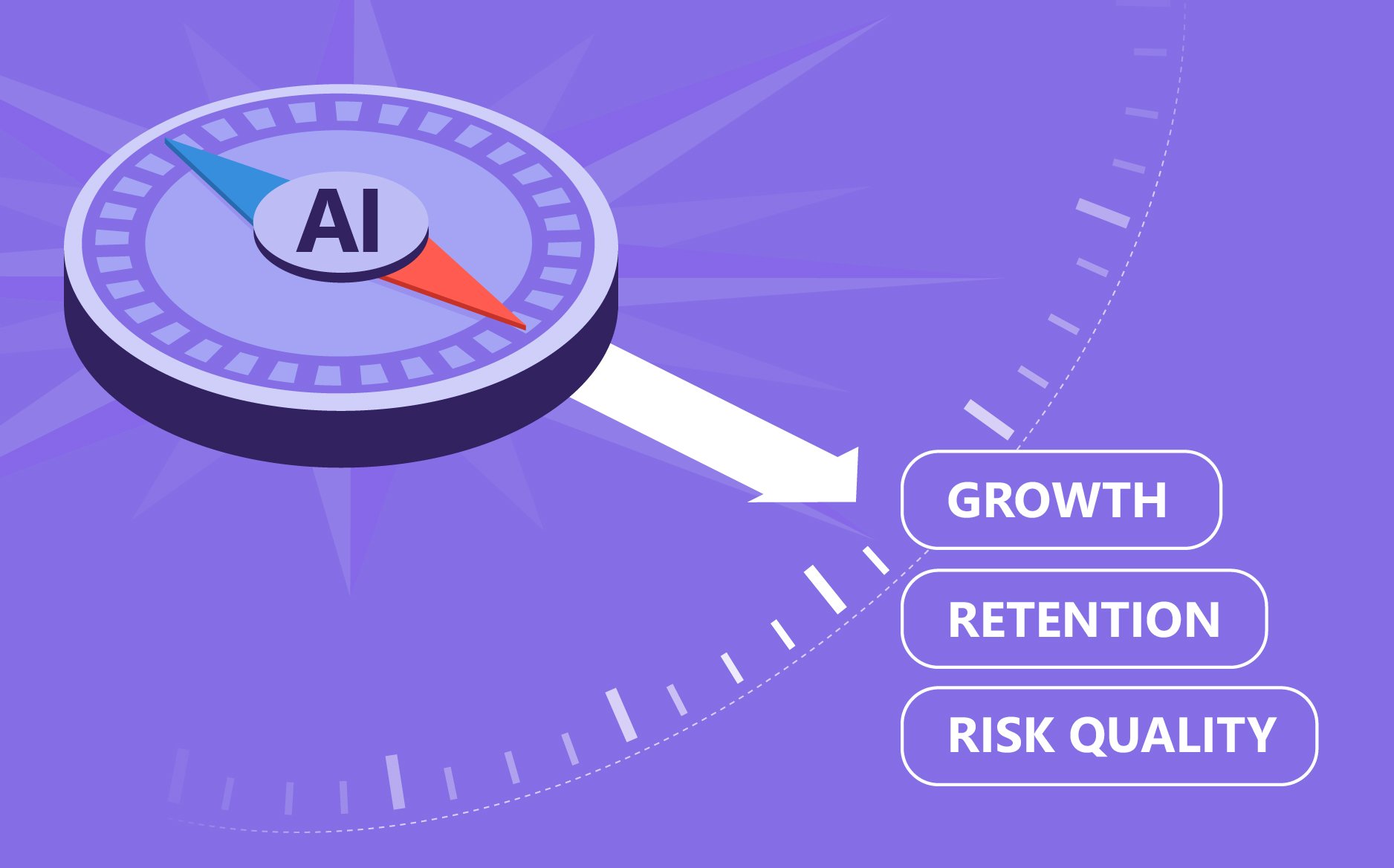

For underwriting leaders, the AI value proposition covers three strategic objectives:

- Growth: Smarter targeting expands small commercial portfolios without proportionate increases in expense ratios.

- Retention: Proactively identifying coverage gaps strengthens trust and improves renewal rates.

- Risk Quality: Real-time monitoring of business changes reduces the likelihood of underinsurance-related disputes and loss severity.

A hybrid approach uses AI to augment human expertise. AI can manage and automate the early stages of the process, such as risk screening, policy explanations in plain language, and generating baseline quotes. Human underwriters then step in to review complex cases, make judgment-driven decisions, and ensure high quality standards. This approach empowers insurers to scale efficiently, serve small commercial accounts profitably, and maintain the oversight necessary to protect portfolio integrity.

Industry Implications: Beyond Technology

The integration of AI into small commercial insurance underwriting carries wider implications for our industry:

- Distribution: Independent agents are using AI tools to reach more prospects and offer better education at scale, while direct-to-consumer carriers are finding success in automating quoting and onboarding.

- Underwriting: AI enables underwriters to focus on complex middle-market risks while still profitably serving small accounts through automation. This improves talent allocation across the book of business.

- Competition: Small commercial is one of the most contested segments, with traditional players such as The Hartford and Travelers competing against Next Insurance, Lemonade, and other digital natives. Insurers that move quickly to integrate AI into their workflows will boost their opportunities to capture market share.

- Customers: Small business owners are possibly the greatest beneficiaries of insurance AI adoption in underwriting, receiving faster quotes, clearer explanations of coverage, and policies that support and enable their business’s growth.

The underinsurance crisis in small commercial business represents both a risk and an opportunity. If left unaddressed, it threatens policyholders’ resilience and carriers’ reputations. For insurers willing to invest in AI-driven efficiency, however, it provides a path to profitable growth, improved customer outcomes, and stronger long-term retention.

Carriers have two clear opportunities. Internally, AI can transform underwriting, distribution, claims, and servicing processes, making small commercial accounts economically viable despite their lower premiums. Externally, the sheer volume of underinsured small businesses represents one of the largest untapped markets in the industry.

The question is no longer whether the gap exists – it does and it is significant. The real question is: which insurers will do the legwork, apply technology, and position themselves as a trusted partner for America’s small businesses? Those who act now will not only strengthen their books of business but also secure a durable competitive advantage in one of the industry’s most critical growth segments.

Want to benchmark where your peers really stand with AI today? Download the State of AI Adoption in Insurance 2025 report for exclusive insights, trends, and data to guide your strategy.